How Big Is the Automotive Optic Lenses Safety System Market?

Automotive Optic Lenses Safety System Market: Growth, Trends, Drivers, Challenges, Segmentation, and Competitive Analysis

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-optic-lenses-safety-system-market/request-sample

Market Size

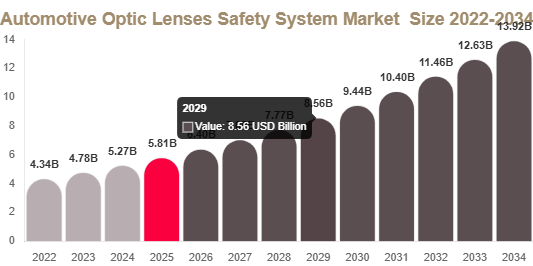

The global Automotive Optic Lenses Safety System Market size was valued at USD 5.8 billion in 2025 and is projected to reach USD 6.4 billion in 2026.

The market is forecasted to reach approximately USD 13.9 billion by 2034, expanding at a CAGR of 10.2% during the forecast period of 2025–2034.

Introduction

The Automotive Optic Lenses Safety System Market is expanding rapidly due to the rising integration of advanced driver assistance systems (ADAS), autonomous driving technologies, and camera-based vehicle safety solutions. These optical lens systems are essential for enabling clear vision, object detection, and real-time monitoring in modern vehicles.

Automotive optic lenses are widely used in ADAS cameras, driver monitoring systems, parking assistance systems, night vision modules, and autonomous driving platforms. Increasing vehicle safety regulations and growing demand for intelligent mobility systems are accelerating adoption across passenger, commercial, and electric vehicles.

Market Drivers

Expansion of ADAS Deployment Across Vehicles

The growing adoption of ADAS technologies is one of the strongest drivers of the Automotive Optic Lenses Safety System Market. Features such as lane departure warning, adaptive cruise control, and collision avoidance depend on high-quality optical lenses.

Automakers are increasingly integrating ADAS features across economy and mid-range vehicles, not just luxury segments. Regulatory mandates for vehicle safety are further accelerating the deployment of camera-based systems, increasing demand for precision optical lenses.

Rapid Growth of Electric and Autonomous Vehicles

The expansion of electric and autonomous vehicles is significantly boosting market growth. These vehicles rely heavily on advanced imaging systems to monitor surroundings, detect obstacles, and ensure safe navigation.

Autonomous vehicles require multiple high-resolution cameras and optical lenses to process real-time environmental data. Similarly, electric vehicles integrate smart safety systems that depend on advanced optical technologies, driving long-term demand.

Market Challenges

High Cost of Advanced Optical Systems

One of the key challenges in the market is the high cost of manufacturing automotive-grade optical lenses. These components require precision engineering, advanced coatings, and thermal resistance, which increases production costs.

As a result, integration of advanced optical safety systems is often limited to premium and mid-range vehicles, slowing adoption in cost-sensitive markets.

Increasing Shift Toward Fully Digital Systems

The automotive industry is gradually shifting toward fully digital instrument and vision systems. This transition may reduce reliance on traditional optical lens-based systems in certain applications.

However, high-performance safety and ADAS systems still depend on optical lenses, balancing the impact of this shift.

Market Opportunities

Growth of Autonomous Commercial Fleets

The rise of autonomous commercial vehicles presents a major opportunity for the Automotive Optic Lenses Safety System Market. Logistics companies and mobility providers are investing in camera-heavy systems for navigation and safety monitoring.

These vehicles require durable, high-resolution optical lenses capable of functioning in complex driving environments, creating strong long-term demand.

Expansion in Emerging Automotive Markets

Developing regions are increasingly adopting vehicle safety technologies due to stricter regulations and rising consumer awareness. Countries in Asia Pacific, Latin America, and the Middle East are integrating ADAS features into mid-range vehicles.

This is significantly expanding the market base for automotive optical lenses across cost-sensitive automotive segments.

Segmental Analysis

By Lens Type

Wide-angle lenses dominated the market with a share of 38.42% in 2025. These lenses are widely used in surround-view cameras, parking assistance systems, and blind spot detection applications due to their broad field of view.

Infrared lenses are expected to be the fastest-growing segment with a CAGR of 12.3%. These lenses are widely used in night vision systems and driver monitoring applications, improving safety in low-light conditions.

By Application

ADAS camera systems accounted for the largest share of 44.27% in 2025. These systems rely heavily on optical lenses for features like lane detection, collision avoidance, and adaptive cruise control.

Driver monitoring systems are expected to grow at a CAGR of 11.9%, driven by rising concerns about driver fatigue and distracted driving.

By Vehicle Type

Passenger vehicles dominated the market with a share of 63.11% in 2025. Increasing demand for safety features and connected mobility systems is driving adoption in this segment.

Commercial vehicles are expected to grow at a CAGR of 10.8% due to increasing adoption of fleet safety systems and autonomous logistics solutions.

Regional Insights

North America held 35.18% market share in 2025 due to strong adoption of ADAS technologies and autonomous vehicle development.

Asia Pacific is expected to be the fastest-growing region with a CAGR of 11.84%, driven by high vehicle production and increasing EV adoption.

Europe continues to grow steadily due to strict safety regulations and strong automotive manufacturing capabilities.

Competitive Landscape

The Automotive Optic Lenses Safety System Market is highly competitive, with global automotive suppliers and electronics companies investing in advanced imaging technologies.

Key Players Analysis

- Robert Bosch GmbH

Robert Bosch GmbH is a leading player offering advanced ADAS and automotive sensing technologies, including optical imaging systems. - Continental AG

Continental AG focuses on intelligent mobility solutions and integrated camera-based safety systems. - Denso Corporation

Denso Corporation develops high-precision automotive components, including optical and sensor-based safety systems. - Magna International Inc.

Magna is investing in advanced vehicle safety technologies and camera-based systems for autonomous driving. - Valeo SA

Valeo specializes in automotive vision systems and advanced driver assistance technologies. - Aptiv PLC

Aptiv focuses on connected vehicle systems and intelligent safety solutions. - Panasonic Automotive Systems Co., Ltd.

Panasonic develops advanced imaging and sensor technologies for automotive applications. - HELLA GmbH & Co. KGaA

HELLA is known for its lighting and electronic systems, including optical safety components. - ZF Friedrichshafen AG

ZF specializes in mobility systems and ADAS technologies. - Mobileye Global Inc.

Mobileye is a leader in autonomous driving vision systems and camera-based safety technologies.

Conclusion

The Automotive Optic Lenses Safety System Market is set for strong growth driven by rising adoption of ADAS, autonomous vehicles, and advanced camera-based safety systems. While cost challenges and digital transformation trends may create pressure, increasing demand for vehicle safety and intelligent mobility will continue to drive expansion.

Manufacturers focusing on innovation, precision optics, and integration with AI-based vehicle systems are expected to gain a strong competitive advantage in the evolving automotive landscape.

Get Your Sample Report Here: https://www.redlinepulse.com/report/automotive-optic-lenses-safety-system-market/request-sample