Vehicle Embedded Software Market: Key Drivers, Challenges, and Opportunities

Vehicle Embedded Software Market Overview

The Vehicle Embedded Software Market is witnessing strong growth due to rapid adoption of software-defined vehicles, increasing integration of connected systems, and rising demand for advanced driver assistance and infotainment technologies across modern automotive platforms. Embedded software plays a critical role in managing vehicle functions such as ADAS, telematics, battery management systems, powertrain control, and autonomous driving capabilities. According to Redline Pulse, the market is expanding rapidly as automakers shift toward centralized computing architectures and intelligent mobility ecosystems.

The increasing demand for connected vehicles, over-the-air updates, and digital cockpit experiences is pushing automotive manufacturers to invest heavily in embedded software development. Electric vehicles are further accelerating this demand as they require advanced software systems for energy optimization, thermal management, and battery performance monitoring. In addition, regulatory pressure on safety, emissions, and cybersecurity is strengthening the need for highly reliable embedded software solutions across all vehicle categories.

Get Sample Report Here: https://www.redlinepulse.com/report/vehicle-embedded-software-market/request-sample

Buy Now Report: https://www.redlinepulse.com/report/vehicle-embedded-software-market/buy-now

View Full Report: https://www.redlinepulse.com/report/vehicle-embedded-software-market

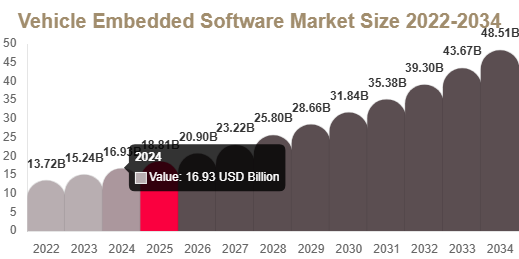

Vehicle Embedded Software Market Size and Growth Outlook

The Vehicle Embedded Software Market was valued at USD 18.7 billion in 2025 and is projected to reach USD 20.9 billion in 2026. By 2034, the market is expected to attain USD 48.6 billion, growing at a CAGR of 11.1% during the forecast period from 2025 to 2034.

This strong growth is driven by increasing deployment of software-defined vehicle platforms, rising adoption of electric mobility, and expanding demand for connected vehicle ecosystems. Automotive manufacturers are increasingly focusing on integrating intelligent software frameworks that support real-time communication between sensors, ECUs, and cloud systems, improving both safety and driving efficiency.

Market Drivers

Rising Adoption of ADAS and Safety Systems

The increasing integration of advanced driver assistance systems is one of the major drivers of the Vehicle Embedded Software Market. Features such as adaptive cruise control, lane departure warning, automatic emergency braking, and collision avoidance rely heavily on embedded software for real-time data processing and decision-making.

Expansion of Connected Vehicle Ecosystems

Connected vehicles are becoming increasingly popular due to demand for smart mobility solutions. Embedded software enables communication between vehicles, cloud platforms, mobile applications, and infrastructure systems, enhancing navigation, telematics, and predictive maintenance capabilities.

Growth of Electric Vehicles

The rapid adoption of electric vehicles is significantly boosting demand for embedded software solutions. EVs require advanced software for battery management, charging optimization, energy efficiency, and thermal control systems, making embedded software a core component of electric mobility platforms.

Market Challenges

Cybersecurity and Software Complexity

The increasing complexity of vehicle software systems creates major cybersecurity risks. Modern vehicles contain millions of lines of code, making them vulnerable to cyberattacks. Ensuring software security across connected platforms remains a key challenge for manufacturers.

High Development and Integration Costs

Developing and integrating embedded software across multiple vehicle systems requires significant investment. OEMs and suppliers face high costs related to testing, validation, and compliance with global automotive standards.

Regulatory Compliance Pressure

Automotive software must comply with strict safety, emissions, and cybersecurity regulations across different regions. Meeting these requirements increases development timelines and operational complexity.

Market Opportunities

Expansion of Autonomous Driving Technologies

The development of autonomous vehicles presents significant opportunities for embedded software providers. These systems rely on real-time data processing, sensor fusion, AI algorithms, and vehicle control software to enable self-driving capabilities.

Growth of Over-the-Air Software Updates

OTA update systems are becoming standard in modern vehicles, allowing manufacturers to remotely upgrade features, fix bugs, and enhance performance. This is creating continuous demand for scalable embedded software platforms.

Segment Analysis

By Software Layer

The market includes operating systems, middleware, and application software. Operating systems dominate due to their critical role in managing vehicle hardware and software integration, while middleware is growing rapidly due to its ability to connect multiple vehicle systems efficiently.

By Vehicle Type

Passenger vehicles dominate the market due to high adoption of infotainment, ADAS, and connected technologies. However, commercial vehicles are expected to grow at the fastest rate due to fleet digitalization and telematics adoption.

By Application

ADAS and safety systems hold a major share due to increasing safety regulations, while infotainment and connectivity applications are growing rapidly due to consumer demand for digital vehicle experiences.

By Deployment Type

Embedded onboard software dominates due to widespread adoption in traditional automotive systems, while cloud-integrated software is expanding rapidly with the growth of connected vehicle ecosystems.

Regional Analysis

North America holds a strong market position due to advanced automotive technology adoption and strong EV infrastructure. Europe is driven by strict regulatory standards and high demand for sustainable mobility solutions. Asia Pacific is the fastest-growing region due to large-scale vehicle production in China, India, and Japan. Latin America and Middle East & Africa are also witnessing steady growth supported by rising automotive digitalization and infrastructure development.

Competitive Landscape and Key Players

The Vehicle Embedded Software Market is highly competitive, driven by innovation, partnerships, and increasing investment in automotive software platforms.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Aptiv PLC

- NXP Semiconductors

- Infineon Technologies AG

- Panasonic Holdings Corporation

- BlackBerry Limited

- Elektrobit Automotive GmbH

- NVIDIA Corporation

These companies are focusing on AI-driven software systems, cybersecurity integration, cloud-based vehicle platforms, and autonomous driving technologies. Strategic collaborations with OEMs and semiconductor companies are accelerating development of next-generation software-defined vehicles.

Conclusion

The Vehicle Embedded Software Market is expected to witness strong growth during 2025–2034, driven by rising demand for connected vehicles, electric mobility, and autonomous driving technologies. Despite challenges such as cybersecurity risks and high development costs, continuous innovation in automotive software ecosystems is creating significant opportunities for global players.