Shipbuilding Market Forecast Report Highlighting Emerging Opportunities by 2032

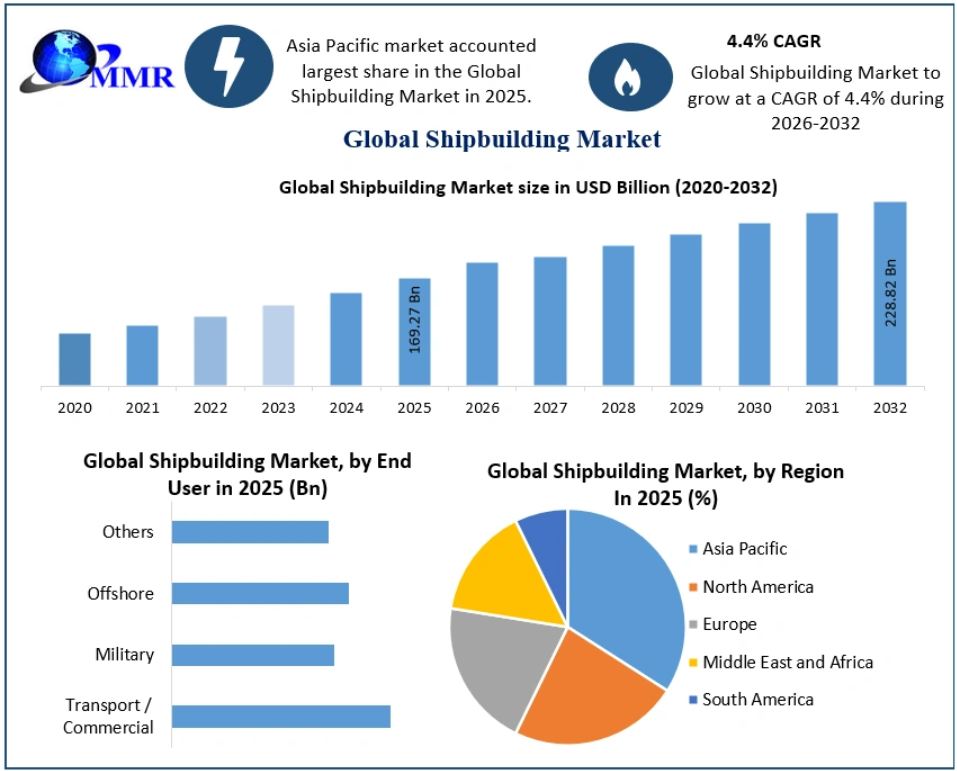

The global Shipbuilding Market is experiencing strong momentum as international maritime trade, naval modernization programs, and green shipping initiatives continue to reshape the global marine industry. The market was valued at USD 169.27 Billion in 2025 and is projected to reach nearly USD 228.82 Billion by 2032, expanding at a CAGR of 4.4% during the forecast period.

Shipbuilding plays a crucial role in global commerce, supporting more than 90% of worldwide cargo transportation through commercial, naval, offshore, and specialized vessels. The industry encompasses the design, construction, and launching of ships using advanced manufacturing technologies, specialized materials, and modern shipyard infrastructure.

The Asia Pacific region dominates the global shipbuilding ecosystem, led by China with approximately 53% market share, followed by South Korea at 28% and Japan at 12%. The region continues to strengthen its leadership through massive shipyard capacity, government support, technological innovation, and rising investments in green and autonomous vessels.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/148775/

Green Shipbuilding and Digital Transformation Reshape the Industry

The tightening environmental regulations introduced by the International Maritime Organization are significantly accelerating the transition toward sustainable shipbuilding practices. Shipbuilders across Asia, Europe, and North America are increasingly investing in LNG-powered vessels, hybrid propulsion systems, ammonia-ready ships, methanol-fueled vessels, and wind-assisted marine technologies.

The growing demand for environmentally friendly vessels is transforming the competitive landscape of the global shipbuilding industry. LNG carriers, dual-fuel container ships, and energy-efficient commercial vessels are becoming key focus areas for major shipyards.

Digitalization in shipbuilding is also emerging as a transformative trend. Advanced technologies such as AI-powered production planning, robotics, digital twins, automation systems, and 3D printing are helping shipyards improve operational efficiency, reduce construction timelines, and lower manufacturing costs. The increasing adoption of Industry 4.0 technologies is further supporting productivity improvements across modern shipyards.

Autonomous ships and unmanned surface vessels are also gaining traction, particularly in naval and offshore applications. The integration of smart navigation systems, predictive maintenance solutions, and intelligent ship management technologies is expected to create substantial long-term opportunities in the market.

Rising Seaborne Trade and Government Support Drive Market Growth

The steady rise in global seaborne trade remains one of the primary drivers of shipbuilding market growth. Expanding global supply chains, increasing containerization, and growing energy transportation activities are generating strong demand for cargo ships, tankers, LNG carriers, and large container vessels.

Container ships currently represent the dominant ship type segment, accounting for over 34–36% of total new shipbuilding orders in 2025. The rapid growth of e-commerce, global logistics expansion, and demand for mega-container ships are significantly contributing to segment growth. China and South Korea continue to receive the majority of new containership orders, particularly for dual-fuel LNG and methanol-ready vessels.

Governments across major shipbuilding nations are also implementing strategic policies to strengthen domestic maritime industries. Countries including China, South Korea, Japan, and India are offering subsidies, tax incentives, green financing programs, and shipyard modernization initiatives to improve global competitiveness.

India, for example, is targeting a 5% share of the global shipbuilding market by 2032 through investments in shipyard infrastructure, naval expansion, and maritime manufacturing development.

Skilled Labor Shortage and Rising Costs Remain Key Challenges

Despite positive market growth, the industry continues to face challenges related to skilled workforce shortages and rising labor costs. Shipbuilding requires highly specialized expertise in welding, marine engineering, naval architecture, digital manufacturing, and vessel design.

Many traditional shipbuilding countries are experiencing aging workforces and declining vocational training participation, creating talent shortages across shipyards. Labor costs in regions such as Europe, Japan, South Korea, and North America have increased significantly over the past five years, reducing cost competitiveness against Chinese shipbuilders.

The increasing adoption of AI, automation, and digital manufacturing technologies is also widening the skills gap, as shipyards require advanced technical professionals capable of managing intelligent production systems and smart ship technologies.

Steel Continues to Dominate Material Usage in Shipbuilding

Steel remains the dominant material used across the global shipbuilding industry, accounting for more than 85% of total shipbuilding materials in 2025. Marine-grade steel is widely preferred due to its structural strength, durability, impact resistance, and cost efficiency.

Global consumption of marine-grade steel exceeded 23 million tonnes in 2025, with China contributing nearly 45% of global shipbuilding steel demand. Advanced high-tensile steel grades are increasingly being used in LNG carriers and large-capacity container vessels to improve fuel efficiency while maintaining structural integrity.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/148775/

Asia Pacific Maintains Global Leadership in Shipbuilding

The Asia Pacific region continues to dominate the global shipbuilding market, accounting for more than 93% of worldwide ship production. China remains the world’s largest shipbuilder, producing over 36 million gross tons of merchant vessels in 2025 and securing nearly 70% of global shipbuilding orders.

China continues to strengthen its maritime dominance through state-backed shipbuilding programs, massive shipyard capacity, and advanced manufacturing investments. Chinese shipyards exported nearly 75% of their production to international buyers, further reinforcing the country’s leadership in global maritime trade.

South Korea remains highly competitive in high-value vessels such as LNG carriers and technologically advanced eco-friendly ships. Major South Korean shipbuilders continue to lead innovation in AI-enabled ship intelligence and ammonia-ready vessel technologies.

Japan maintains strong expertise in specialized and energy-efficient vessel construction, particularly hybrid propulsion systems and autonomous ship technologies.

Emerging shipbuilding nations such as India, Vietnam, and the Philippines are also expanding their shipyard capabilities and increasing investments in maritime infrastructure to capture greater global market share.

Recent Industry Developments Accelerate Technological Innovation

The global shipbuilding industry continues to witness major technological advancements and strategic consolidation activities.

In September 2023, HD Hyundai Heavy Industries introduced its HCX-23 trimaran naval vessel concept featuring stealth technologies, drone support systems, retractable radar systems, and laser weapon integration. The vessel represents a significant advancement in next-generation naval shipbuilding and autonomous maritime defense technologies.

In July 2025, China State Shipbuilding Corporation and China Shipbuilding Industry Corporation moved toward completing a major merger valued at approximately USD 16 Billion. The combined entity is expected to become the world’s largest shipbuilding conglomerate, with assets exceeding USD 56 Billion and annual revenue of nearly USD 18 Billion.

The merger further strengthens China’s leadership position in both commercial and naval shipbuilding markets while increasing the country’s influence over global shipbuilding supply chains.

Competitive Landscape

The global shipbuilding market remains highly consolidated, with major Asian companies dominating commercial and naval vessel production. Leading market participants are focusing on LNG vessels, autonomous ships, AI-enabled shipbuilding, hybrid propulsion systems, and digital shipyard modernization to strengthen their competitive positions.

Key players operating in the global Shipbuilding Market include:

- HD Hyundai Heavy Industries

- Samsung Heavy Industries

- Hanwha Ocean

- China State Shipbuilding Corporation

- Jiangnan Shipyard

- Mitsubishi Heavy Industries

- Fincantieri

- Damen Shipyards Group

- Cochin Shipyard Limited

- Mazagon Dock Shipbuilders Limited

The growing focus on sustainable maritime transport, digital shipbuilding technologies, autonomous vessels, and naval modernization programs is expected to drive continuous innovation and long-term growth across the global Shipbuilding Market through 2032.